The Liquidity Gap: What’s Really Happening Inside Indonesian Crypto Exchanges

If you’ve ever tried to buy BTC on a local Indonesian exchange and felt something was off, you probably weren’t imagining things. You hit buy at a price that looked fine, but by the time the order filled, you were already slightly in the red.

It’s a common frustration, but it usually isn’t the exchange trying to “get” you. It’s actually a symptom of the infrastructure running behind the scenes.

That infrastructure is market making. Understanding how it works explains pretty much everything about where the Indonesian crypto market stands today—and where it needs to go next.

The hidden cost of every trade

Every time you trade, you pay two costs. The first is obvious: the fee shown on your screen. The second is hidden, but often much more expensive: the spread.

Think of it like this: at any given second, there’s a gap between what sellers want and what buyers are willing to pay. That gap is the bid-ask spread. When you buy “at market,” you pay the higher price. When you sell, you get the lower one. You’re absorbing that cost on every single trade, whether you realize it or not.

In massive, global markets, this gap is tiny—barely a fraction of a percent. But in younger markets like Indonesia, that gap is wider. It’s not malicious; it’s just that the machinery required to keep those prices tight hasn’t been fully built yet.

Who is actually tightening the spread?

In a high-volume market, the spread compresses on its own. When people are trading constantly, competition for the best price naturally closes the gap.

But younger markets need a jumpstart. That’s where market makers come in. Their entire job is to constantly put out buy and sell orders to keep the order book from thinning out. They make money from the spread itself, but in exchange, they provide a service: your orders fill faster and at prices that aren’t wildly different from the global average.

This isn’t just a passive thing. Exchanges have actual contracts with these firms. There are strict rules about how wide the spread can be, how much “depth” (available crypto) must be on the books, and how quickly they have to get back online if the market gets crazy.

If a market maker pulls their orders or widens the spread when things get volatile—exactly when you need them most—they aren’t doing their job. Managing this relationship is one of the most important things an exchange does, though most users never see it happening.

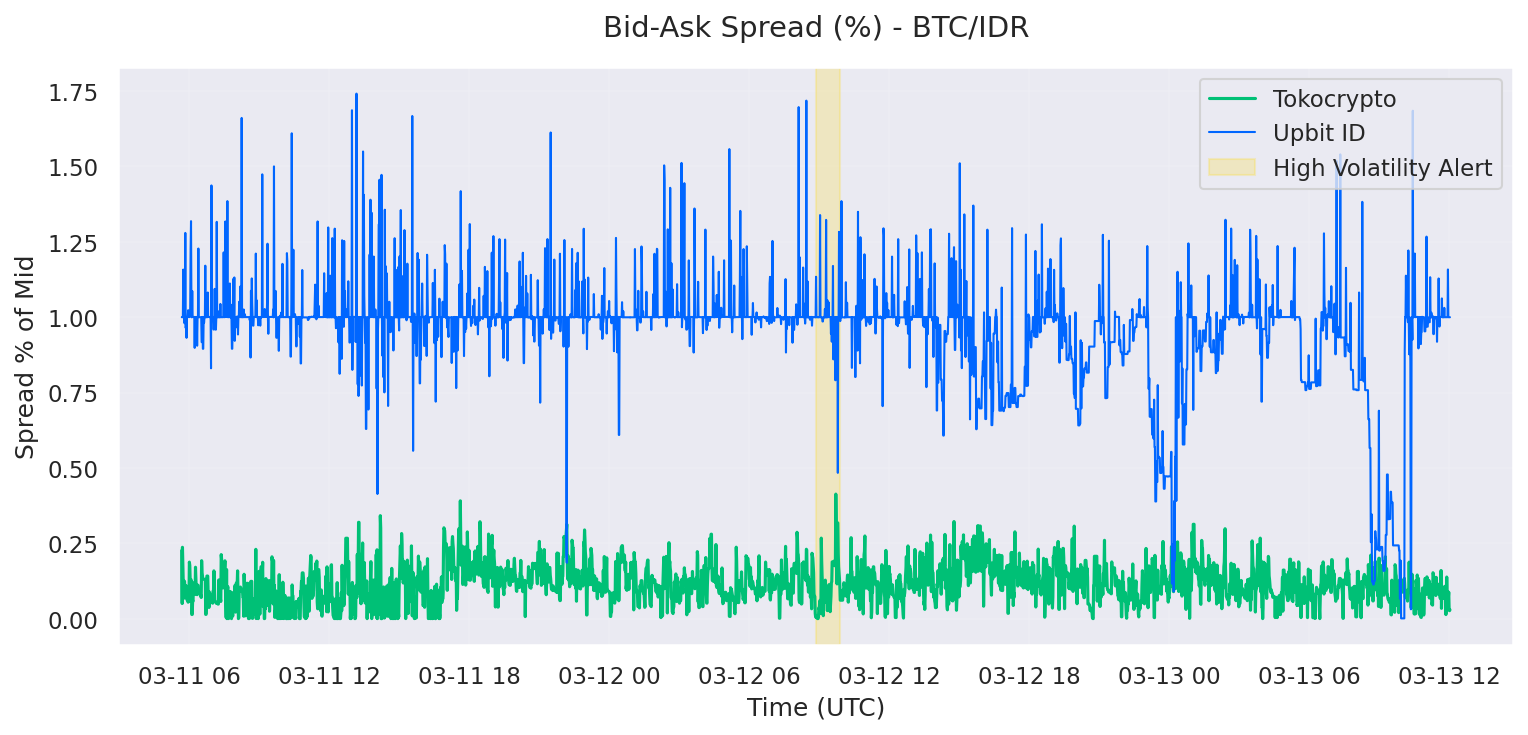

What the data actually looks like

I wanted to see this for myself, so I built a tool to track it. I polled live order book data from Indonesian exchanges every minute for 54 hours straight. This gave me thousands of snapshots showing exactly how local liquidity behaves.

The results show a market that is clearly in transition.

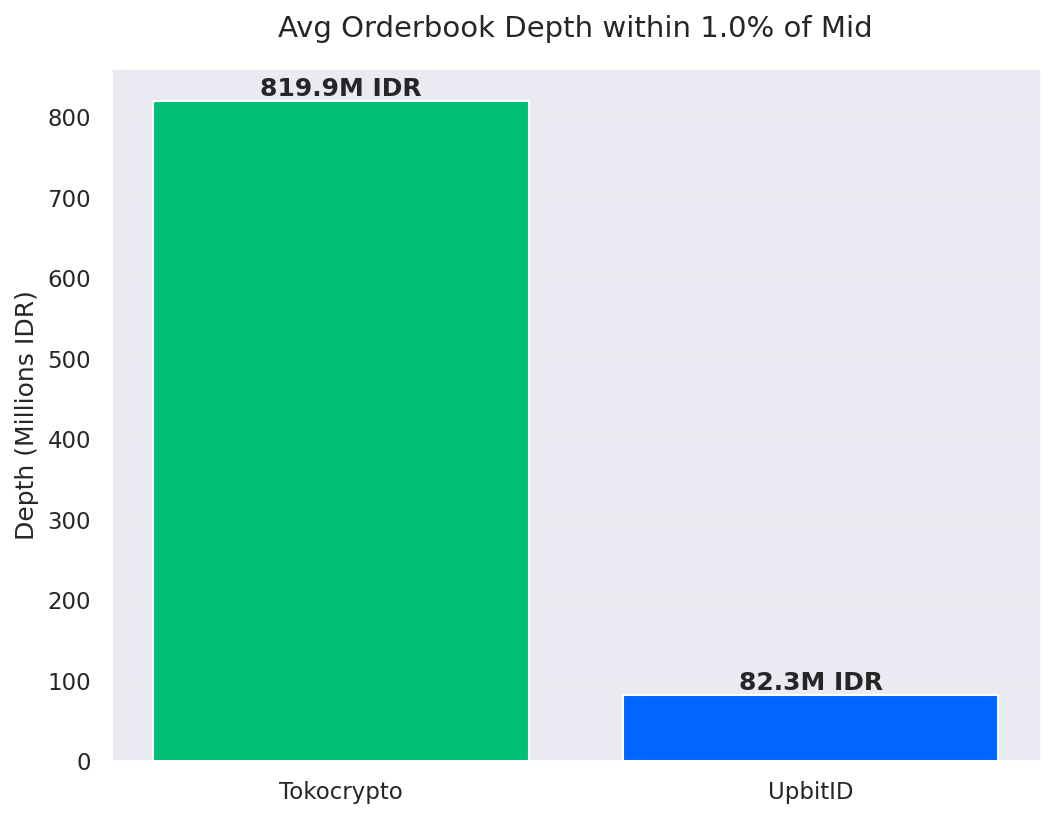

One exchange was clearly being managed. It had about 820 million IDR (~$51K USD) of depth within 1% of the price, a tight spread (4.2 basis points), and orders were present 95% of the time. You can see the professional touch here—the book is being actively maintained, not just left to grow on its own.

The other exchange was a different story. It had only about 82 million IDR (~$5K USD) at that same 1% threshold, with a spread that was four times wider. The depth was fragmented, which usually means the only people trading are ordinary users. It’s an early-stage market, not a broken one.

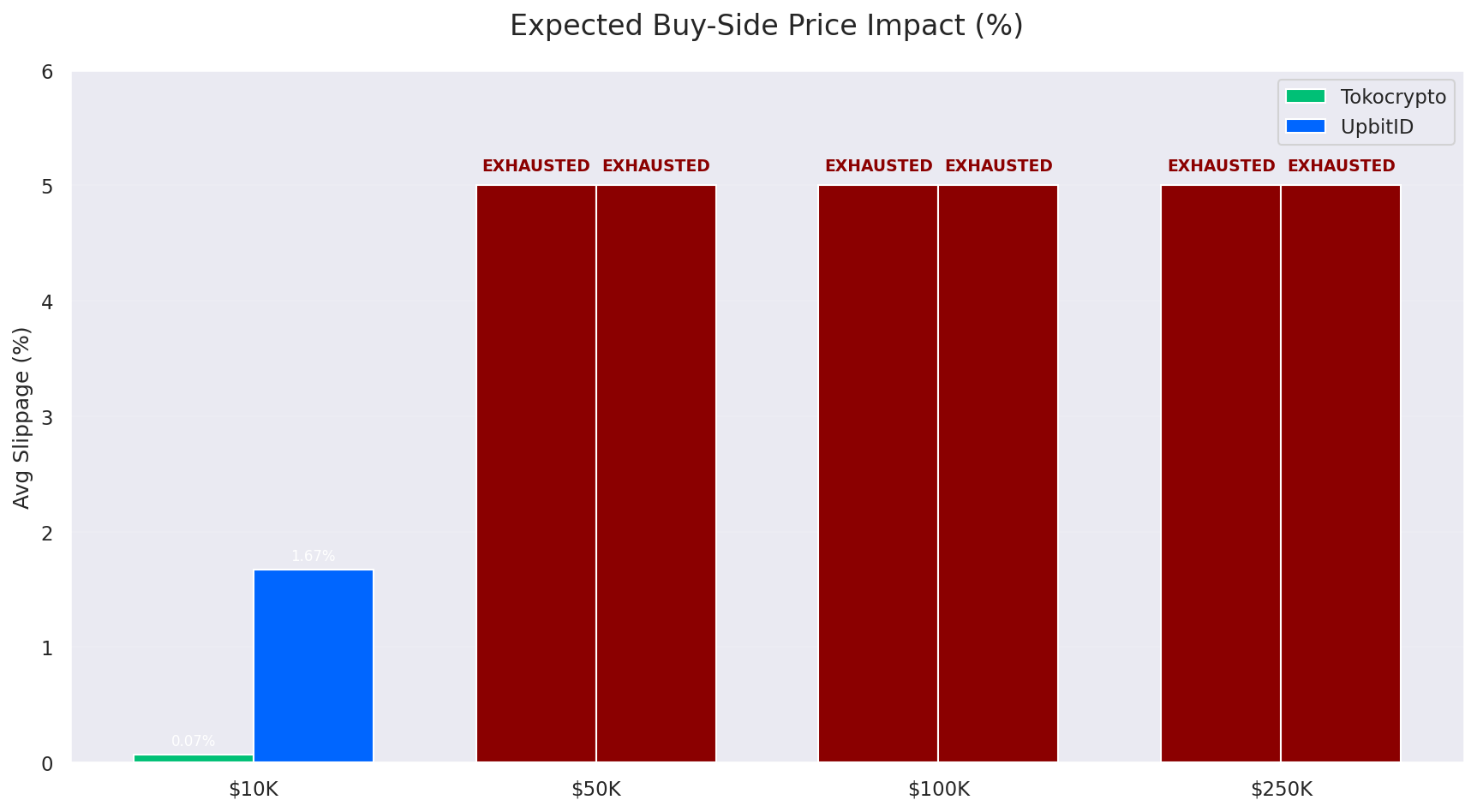

The slippage data makes this even clearer:

If you try to drop $10,000 USD into either of these exchanges, you’ll likely eat through all the available liquidity. This is the ceiling for Indonesian crypto right now. It’s what stands between where we are today and the kind of serious capital needed for the next level.

Why this matters for Indonesia

The differences we’re seeing aren’t just random. They are the direct result of how much an exchange is willing to invest in its infrastructure—specifically, how they handle market making.

OJK regulations have made the Indonesian market much more legitimate, but they’ve also made things harder for the exchanges. Dealing with IDR settlement and local counterparty rules takes real effort.

Exchanges have to decide when organic trading is enough and when they need to hire professionals to keep things deep. And more importantly, they need to hold those professionals accountable when things go sideways.

The exchanges that solve this first—the ones that keep spreads tight even when the market is crashing—will be the ones that win over the traders who currently use global platforms for active trading.

The data shows this gap is starting to close. One exchange is already operating at a professional tier. The other is just one good infrastructure decision away from doing the same.

The big picture

The market structure in Indonesia is maturing faster than most people realize. The fact that I can even run this analysis—because the data is transparent and available—is a great sign for the ecosystem.

The next phase isn’t about matching global prices. It’s about building the “plumbing” that makes local exchanges the natural choice for anyone trading in IDR.

Market making is the heart of that plumbing. Figuring out how to do it right is one of the more interesting challenges in Indonesian fintech right now.

*Methodology, full dataset, and the interactive tool I used are all on the project page. You can also find the raw code on GitHub.